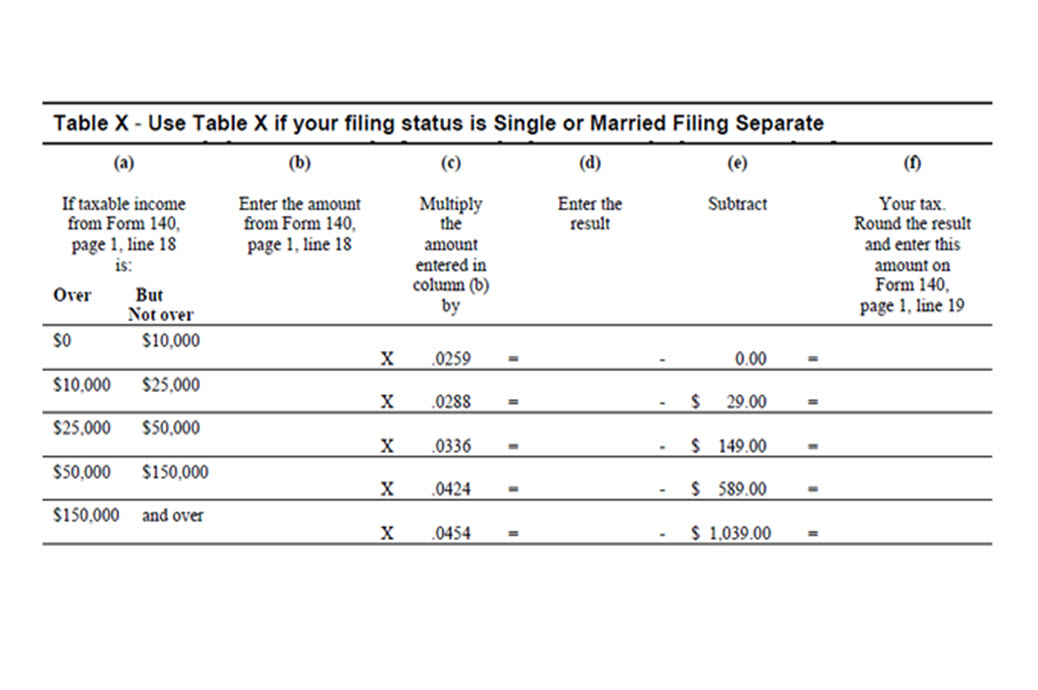

Most states in the US have some type of graduated income tax. This means that as your taxable income increases, the higher amounts of income are taxed at a higher and higher rate. There are several ways to express the relationship between taxable income and the corresponding amount of tax. In the state of Arizona, the instructions for Form 140 includes the table above for individuals filing single or married and filing single.

Column b represents your taxable income. Columns c, d, and e tell you what to do with that income to find your tax. Once the calculation is made, the corresponding tax is calculated in column f.

Let’s think of the relationship in this table as a function T(x) where x is the taxable income from line 18 of Form 140. If I write T(8,000), I am referring to the tax on a taxable income of 8,000. This taxable income level falls in the interval over 0, but not over 10,000. In this interval, the tax is calculated by multiplying the taxable income by 0.0259 to give,

T(8000) = 0.0259(8000) = 207.20

If we want to find the tax on a taxable income of 45,000, note that this income is over 25,000, but not over 50,000. To calculate the tax, we must multiply the income by 0.0336 and subtract 149. When we do this, we get

T(45,000) = 0.0336(45000) – 149 = 1363

Looking at T(8000) and T(45000) where specific values of x were supplied, we see that we could use the formula 0.0259x or 0.0336x – 149 to compute the tax. As long as we know when each formula is applicable, we can apply the formula appropriately. This is exactly what the right side of a piecewise function does.

Knowing when to apply the formulas from the table above, we can come up with linear functions for each range of taxable incomes. Using these formulas, we can write the piecewise function,