How do you make an amortization table?

An amortization table (also called an amortization schedule) records the portion of the payment that applies to the principal and the portion that applies to interest. Using this information, we can determine exactly how much is owed on the loan at the end of any period.

Amortization tables are useful when a loan is to be paid off. Recall that when we calculated the payment, we rounded the amount of the payment up to the penny. Over the term of the loan, we might pay an additional amount each month leading to the principal being reduced more quickly than anticipated. When the final loan payment is made, it needs to be adjusted to insure the balance is paid off properly. Different lenders round payments and interest differently. This may lead to slightly different numbers in the amortization table.

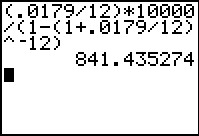

Suppose you want to borrow $10,000 for an automobile. Navy Federal Credit Union offers a loan at an annual rate of 1.79% amortized over 12 months. The payment would be

Since payments are made to the penny, a payment of $841.44 would lead to an overpayment of almost a half of a penny. While this may not seem like much, over the term of the loan it can add up. Financial institutions need to accurately account for these small amounts to insure their books are balanced. An amortization table helps them to do this.

Amortization tables generally have five columns. These columns track the payment number, the amount of the payment, the interest paid in the payment, the portion of the payment applied to the balance, and the outstanding balance on the loan after the payment is made. Let’s look at how the amounts in the table are calculated. We’ll do this by looking at the different rows of the table, one at a time.

The first row of the table helps us to establish the initial balance on the loan. We call it payment 0 since it does not correspond to an actual payment. Using this balance, we can determine the portion of the payment, $841.44, that is applied to the balance and the portion that is interest.

The interest in the payment is calculate by multiplying the interest rate per period times the balance at the end of the previous period,

Interest in Payment 1 = 0.0179/12 · $10,000 ≈ $14.92

In this amortization table, we will round interest amounts to the nearest penny. In practice, you should check with the lender to see how they round interest in the table.

Since the amount applied to balance is the difference between the payment and the interest,

Amount in Payment 1 Applied to Balance = $841.44 – $14.92 = $826.52

This amount reduces the balance at the end of the period,

Balance at the End of the First Period = $10,000 – $826.52 = $9173.48

This strategy is also used to fill in the amounts for the second payment. However, in this case, the interest is calculated using the balance after the previous period.

As the balance decreases, the interest also decreases. This means that a larger and larger portion of the payment goes to paying off the balance.

Payments 3 through 11 are carried out in a similar fashion to give the next few rows. Remember, in this table we are rounding interest amounts to the nearest penny.

For the last payment, we need to pay off the outstanding balance of $840.11. This means the amount of the last payment applied to the balance must be $840.11. The interest in the last payment is

Interest in Payment 12 = 0.0179/12 · $840.11 ≈ $1.25

Combining these two amounts gives the amount of the last payment,

Amount of Payment 12 = $840.11 + $1.25 = $841.36

With these amounts, we can complete the amortization table.

If we add the interest amounts, we find the total amount of interest paid is $97.20.

If we round the payment or interest amounts differently, the amortization table yields different amounts of interest. In the next example, we round all payments and interest amounts up to the nearest penny to see how these change the total amount of interest paid.

Example 4 Make an Amortization Table

Suppose Navy Federal Credit Union rounds all interest and payment amounts up.

a. Find the amortization table on a loan of $10,000 amortized at an annual rate of 1.79% over 12 months with monthly payments.

Solution The terms of the loan are the same as was described above. If the payment is rounded up, we still get a payment of $841.44. When we carry out the process described earlier, we get the table below.

In this table, several of the payments include a slightly higher amount of interest. This means that less of the payment goes towards the outstanding balance. This amount is made up in the last payment where $840.19 is paid to bring the balance to zero. This causes the final payment to be slightly higher.

b. Add the interest amount in the third column to find the total amount of interest paid.

Solution The sum of the interest amounts is $97.29. This is slightly higher than when interest amounts are rounded to the nearest penny. This is to be expected since we rounded all interest amounts up.

The payments and interest amounts may be rounded to the nearest penny, rounded up to the nearest penny, or rounded down to the nearest penny. In all cases, any discrepancies are made up in the final payment.