A couple of you have had trouble finding the payment properly. I am not sure whether this is a calculator issue (there is a screen capture for the payment in Question 3 of Section 5.4) or a formula issue. Often I see people using the interest rate for i instead of the interest rate per period. Remember, since i is the interest rate per period you need to divide it by the number of periods in a year.

Here is an additional example of finding the payment and then using it to construct an amortization table.

Let’s look at a loan problem to see where the payment and amortization table comes from.

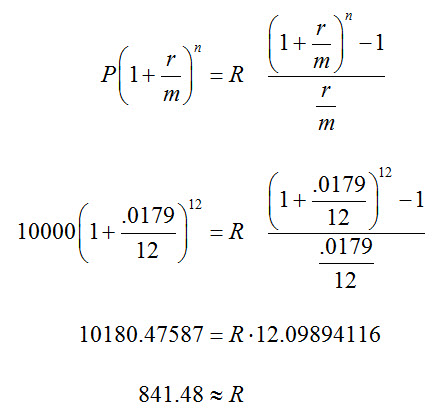

Suppose you want to borrow $10,000 for an automobile. Navy Federal Credit Union offers a loan at an annual rate of 1.79% amortized over 12 months.

a. What are the payments?

To answer this, we need to put the numbers into the appropriate formula and solve for R:

b. Find an amortization table.

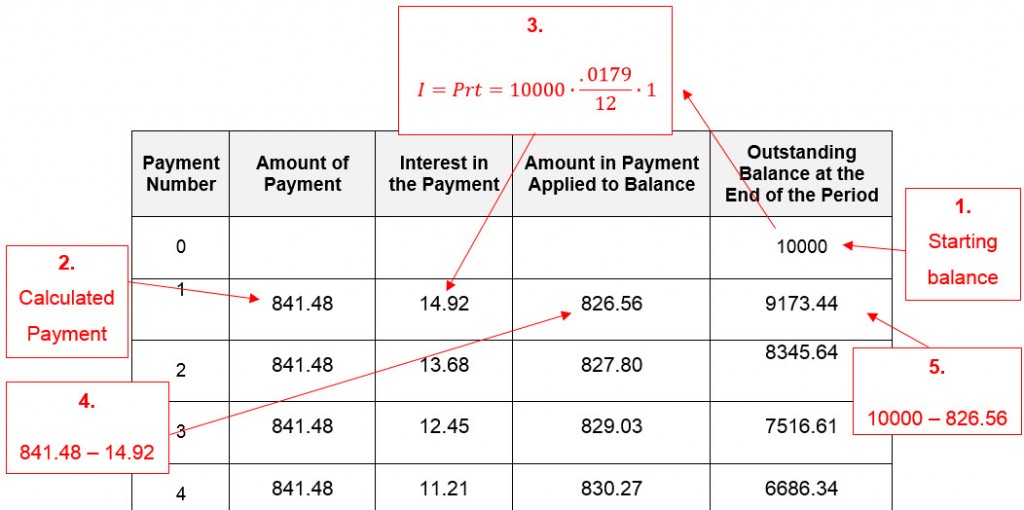

With the payment in hand, we can start filling out the table. Keep in mind that a payment for a credit card is calculated differently. In that case, the minimum payment is the interest plus some percentage of the new balance. In the screens below, you may click on the image for a larger version.

The first few steps consist of filling out Payment 0 and 1:

The interest is calculated with the monthly interest rate of the outstanding balance from the previous period. The amount applied to the balance is the difference between the payment and the interest.

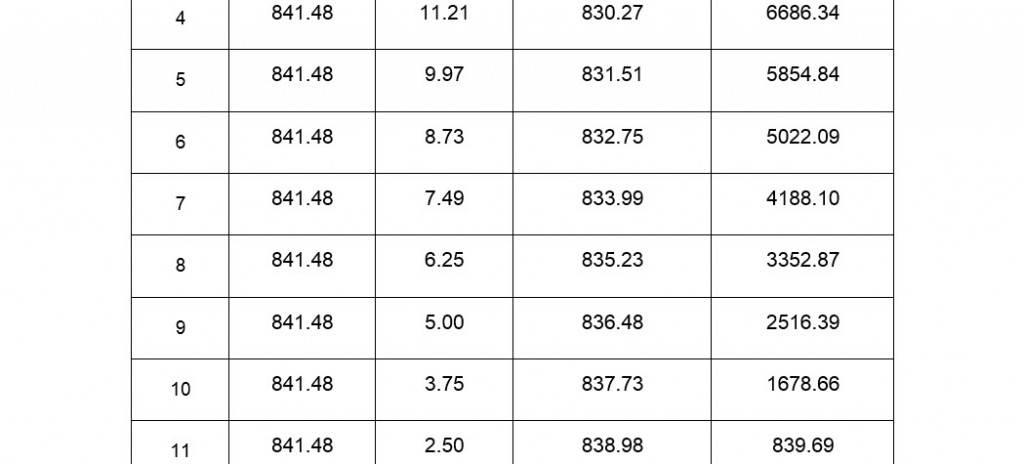

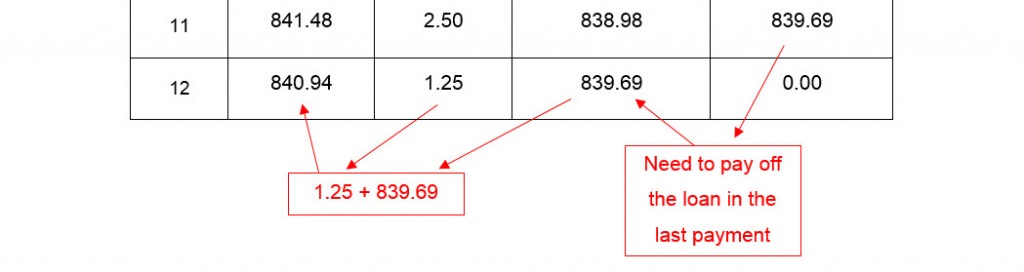

Subsequent rows of the table are calculated in the same way until the final payment.

In the last payment, the principal applied to the balance must be equal to the outstanding balance in Payment 11.

Once that amount applied to the balance is in the 12th payment, then the interest may be calculated, The last payment is then found by adding the interest and the amount applied to the balance.