Decreasing annuities may be used in auto or home loans. In these types of loans, some amount of money is borrowed. Fixed payments are made to pay off the loan as well as any accrued interest. This process is called amortization.

In the language of finance, a loan is said to be amortized if the amount of the loan and interest are paid using fixed regular payments. From the perspective of the lender, this type of loan is a decreasing annuity. The amount of the loan is the present value of the annuity. The payments from the annuity (to the lender) reduce the value of the annuity until the future value is zero.

This interpretation allows us to determine the payment PMT on a loan of PV dollars. Start with the decreasing annuity formula and set the future value FV equal to zero,

This equation is simplified to give

Now solve this equation for the payment PMT:

Payment on an Amortized Loan

Suppose a loan of PV dollars is amortized by periodic payments of PMT at the end of each period. If the loan has an interest rate of i per period over n periods, the payment is

We can use this formula to calculate the payment on any loan that is amortized. Pay special attention to the loan amount. Often the loan amount is not the same as the purchase price because of a down payment. A down payment is an amount paid up front that reduces the amount that must be borrowed. This amount must be subtracted from the purchase price to give the loan amount.

When a loan is amortized for the purchase of a home, the loan is called a mortgage. A typical mortgage is paid back over a 15 or 30 year period with monthly payments.

Example 3 Payment on an Amortized Loan

A young professor purchases a home for $149,000. He plans to take out a 30 year mortgage at an annual interest rate of 5.75%. The mortgage requires a down payment of 20% of the purchase price.

a. Find the monthly payment on this mortgage.

Solution To qualify for this loan, the professor must put 20% down,

Down Payment = 0.20 · 149,000 = 29,800

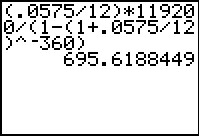

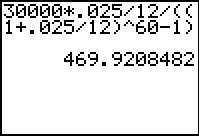

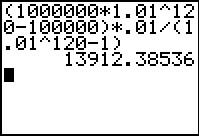

The loan amount is PV = 149,000 – 29,800 = 119,200. For a 30 year mortgage, there are n = 30 · 12 or 360 periods. The interest rate per period is i = 0.0575/12. Using these values, the monthly payment is

This calculation may be carried out on a TI graphing calculator as shown below.

This payment is usually rounded up to the nearest penny to insure the loan is paid off. In practice, this means the final payment will be slightly less than all other payments.

b. How much interest is paid on this mortgage?

Solution According to part a, the professor will pay a total of or $250,423.20 over the term of the loan. Since the loan amount is $119,200, the additional amount paid must be interest,

Interest = $250,423.20 – $119,200 = $131,223.20

The professor pays $131,223.20 in interest on this 30 year mortgage.

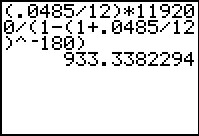

c. The professor has also discovered that he qualifies for a 15 year loan at an annual interest rate of 4.85%. This mortgage also requires a 20% down payment. Find the monthly payment on this mortgage.

Solution For this mortgage, the number of periods is n = 15 · 12 or 180. The intest rate per month is i = 0.0485/12. This leads to a payment of

The calculation is shown below on a TI Graphing Calculator.

Although the interest rate is lower for this mortgage, the shorter term leads to a higher monthly payment of $933.34.

d. How much interest is paid on the 15 year mortgage?

Solution The professor will pay a total of or $168,001.20 in payments. The interest is

Interest = $168,001.20 – $119,200 = $48,801.20

The professor pays $48,801.20 in interest on this 15 year mortgage.

Even though the 15 year mortgage has a lower interest rate, the shorter term leads to higher payments than the 30 year mortgage. However, because of the lower interest rate and shorter term, the amount of interest paid to the lender for the 15 year loan is almost a third of the interest paid on the 30 year loan. In general, loans with shorter terms have lower interest rates. This leads to less interest paid for shorter term loans.

The payments calculated above are the portion of a mortgage payment that applies to the loan. A typical mortgage payment also includes other amounts to cover property taxes, homeowners insurance, and mortgage insurance. These amounts can increase the overall payment by a large amount.

In Section 5.3, we were able to calculate the future value or payments of annuities that were increasing in value or decreasing in value. For an ordinary annuity whose present value is PV, the future value is

if the payments PMT are made into the annuity which earns interest per period i over n periods. Since the payments are made into the annuity, the second term is added. The future value of the annuity increases.

If the payments are made from the annuity, the second term is subtracted to give

In this case, the future value of the annuity decreases since money is removed from the annuity. In some applications, we wish to find the present value (what must be in the account today) so that the account ends up with some amount in the future. The next two examples illustrate how to find the present value in cases like this.

Example 1 Find the Amount Needed to Establish a Trust Fund

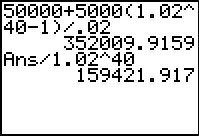

A wealthy individual wishes to create a trust fund for his grandson so that he may withdraw $5000 at the end of every quarter for ten years. At the end of ten years, the grandson will receive the rest of the trust which contains $50,000. If the trust earns 8% interest compounded quarterly, how much should be put into the trust initially?

In this problem, the amount in the annuity is decreasing since withdrawals are being made. However, we wish the future value of the annuity to be $50,000 in ten years. This means that a larger amount must be placed in the trust now so that payment may be made from it. Substitute FV = 50,000, PMT = 5000, i = 0.08/4 = 0.02, and n = 4 · 10 = 40 into

to give

Now solve this equation for the present value.

This is calculated on a TI Graphing Calculator as shown below.

The trust must be established with an initial deposit of $159,421.92.

Example 2 Reaching a Retirement Goal

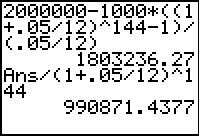

A fifty-five year old investor wishes to retire at age 67. The investor has budgeted $1000 a month that she may deposit in an ordinary annuity that earns 5% interest compounded monthly. If she wishes to accumulate $2,000,000 for retirement, what must be in the account today to reach that goal?

Solution His is an increasing annuity since regular payments are being made an account. Substitute PMT = 1000, i = 0.05/12, n = 12 · 12 = 144 and FV = 2,000,000 into

and solve for the present value PV. This yields

This is calculated on a TI Graphing Calculator as shown below. To simplify the calculation, the numerator is calculated first. Then that answer is divided by the denominator.

There must be $990,871.44 in the annuity today, for the value to grow to $2,000,000 in twelve years.

If the future value of an annuity is fixed, the annuity is called a sinking fund. For instance, you anticipate that you will need $80,000 to fund you child’s education. If you set aside $500 each month in an interest bearing account to reach this goal, you have set up a sinking fund.

In problems involving sinking funds, the future value of the annuity is specified and some other quantity is determined. The formulas used depend on whether the payments are made at the beginning or end of each period.

Example 6 How Long Will It Take To Accumulate Some Amount?

The parents of a newborn child anticipate that they will need $80,000 for the child’s college education. They plan to deposit $500 in an account at the beginning of each month in an account that earns 3% interest compounded monthly. How long will it take them to reach their goal?

Solution This problem specifies a future value of $80,000. Since the payments are made at the beginning of each period, we’ll use the annuity due formula to calculate the length of time it will take to reach the future value.

The payment is R = 500 and the interest rate per period is When these values are put into the annuity due formula, we get

We need to solve this equation for the number of periods n. In doing this, we’ll avoid rounding any number. Rounding too early may lead to large changes in the value of n.

A period of approximately 135 months or a little over 11 years is needed to reach the goal. The number if periods is rounded up to insure the goal is reached. Rounding down would cause the accumulated amount to be slightly less than $80,000.

In some situations, we are interested in determining the payment that will yield a fixed future value.

Example 7 Find The Payment Needed To Accumulate a Fixed Amount

A new car buyer wishes to buy a vehicle with cash in five years. To do this, she wishes to deposit some amount at the end of each month in an account earning 2.5% interest compounded monthly. If she wishes to accumulate $30,000, what should the payments be?

Solution Since the payments are made at the end of each period, we’ll use the future value for an ordinary annuity,

to find the payment. Since the account has a balance of zero to begin with, the present value is zero. She wishes to accumulate $30,000, so FV = 30,000. Over five years, there are n = 12 · 5 or 60 periods with an interest rate per period of . The value of this rate per period is not a terminating decimal so we will use the fraction throughout the calculation. Substitute the values into the formula above to give

This is calculated on a TI Graphing Calculator as shown below.

The payment is rounded up to insure the future value is reached. For this rounded payment, the future value will actually exceed 30,000 by about 58 cents. If the payments were rounded down, the future value would be slightly less than $30,000.

In an ordinary annuity, the payment into the annuity is made at the end of the period. An annuity due differs from this since the payments are made at the beginning of the period. However, we can apply the formula for determining the future value of an ordinary annuity with a little modification. Let’s look at the payments and the interest earned in an annuity due where payments of $1000 are made. As in our earlier example, these payments earn 4% interest compounded semiannually.

The sum of these payments and interest are

This sum contains the term 1000(1.02)6 corresponding to the amount the first payment grows to over six periods. Unlike the sum from a similar ordinary annuity, this sum does not contain a term equal to 1000. This is because the last payment is made at the beginning of the sixth payment period. It earns interest to grow to $1000(1.02) or $1020.

In effect, the future value of an annuity due is like an ordinary annuity with an extra period at the beginning of the annuity and lacking the final payment. This allows us to write the future value for the annuity due.

Future Value of an Annuity Due

If equal payments of PMT are made into an annuity due for n periods at an interest rate of i per period, the future value of the annuity FV is

This formula is almost identical to the future value of the ordinary annuity. The power of n+1 in the numerator incorporates the extra interest earned by the first payment. A payment is subtracted from the ordinary annuity formula to account for the last payment earning interest.

Example 5 Find the Future Value of an Annuity Due

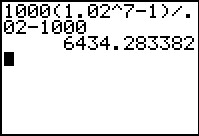

An investor deposits $1000 in a simple annuity at the beginning of each six-month payment period. This annuity earns 4% per year, compounded semiannually. Find the future value if payments are made for three years.

Solution Since the payments are made at the beginning of each period, this is an annuity due. The payment is R = 500 and the interest rate per period is i = 0.05. Since interest is earned semiannually over the term of three years, there are n = 6 periods. Using these values, the future value is

This is calculated on a TI Graphing Calculator as shown below.

This results in the same future value as adding the terms of the sum directly,

Let’s look at an ordinary annuity that is certain and simple. By this, we mean an annuity over a fixed term whose payment period matches the interest conversion period. Additionally, the payments to the annuity are made at the end of the payment period. Suppose a payment of $1000 is made semiannually to the annuity over a term of three years. If the annuity earns 4% per year compounded semiannually, the payment made at the end of the first six-month period will accumulate

This means $1000 is multiplied by 1.02 five times, once for each of the remaining six-month periods.

The next payment also earns interest, but over 4 six-month periods. This payment has a future value of

This process continues until we have the future value for each payment.

The last payment occurs at the end of the last period and earns no interest. Examining each expression for the future value, it appears that there is a pattern to the individual future values. Each future value forms a number corresponding to a geometric sequence.

A geometric sequence is an infinite list of numbers with the form

The amounts above correspond to the first six numbers in the geometric sequence

In this case, a = 1000 and r = 1.02. The numbers in the geometric sequence are called terms. For this geometric sequence, we can number the terms to make them easy to refer to.

In this geometric sequence, each term is 1.02 times larger than the term before it. In fact, the ratio of any two adjacent terms is 1.02. For instance, the ratio of the fourth and fifth terms is

Similarly, the ratio of the first and second terms is

In a geometric series, dividing a term by the preceding one should results in the same number. This number is called the common ratio for the geometric sequence and corresponds to r.

Notice that the power on the 1.02 factor is one less than the term number. This pattern holds in general and leads us to the following pattern.

For any n ≥ 1, the nth term of a geometric sequence is ar n-1.

It might seem as though this general expression might not apply to the first term. In this case, n = 1, so the first term is 1000(1.02)0 or 1000. Other terms may be identified as long as the values for a, r, and n are known.

Example 1 Terms of a Geometric Sequence

Find the fourth and tenth terms of the geometric sequence with a first term 500 and r = 1.05.

Solution If the first term is 500, then a = 500. The fourth term (n = 4) in the geometric sequence is ar3 or 500(1.05)3. This is equal to 578.8125.

The tenth term is 500(1.05)9 ≈ 775.6641.

Let’s continue to look at the future value of a payment of $1000 made semiannually to an annuity over a term of three years. The future value of the annuity FV is the sum of the future values of each payment and corresponding interest is

This sum represents the future value of the annuity. For a sum with few terms, it is easy to add these amounts to give a future value of about $6308.12. This includes six payments of $1000 and interest of $308.12. We can find the same amount using an alternate strategy.

Start by multiplying both sides of the expression for the sum by 1.02 to yield

Subtract the sides of this equation and the previous equation:

Each equation contains identical terms that are highlighted in red. When those terms are subtracted, many terms drop out leaving us with

Each side of this equation may be divided by 0.02 and simplified to yield

This expression yields the same amount as adding the terms directly, $6308.12.

If the payments to the annuity increase in frequency or take place over a longer period of time, it is not convenient to add all of the terms directly. This strategy allows us to find the sum of any number of terms of a geometric sequence.

In the terms of the geometric sequence we have been examining, we can recognize the payment PMT and interest rate per period i. If the payments are paid at the end of n periods, the sum of the accumulated amount of each payment is

Using the strategy, this sum may be written in a simplified form.

Future Value of an Ordinary Annuity

If equal payments of PMT are made into an ordinary annuity for n periods at an interest rate of i per period, the future value of the annuity FV is

We use this expression to calculate the sum when there are any number of terms.

Example 2 Find the Future Value of the Annuity

An investor deposits $500 in a simple annuity at the end of each six-month payment period. This annuity earns 10% per year, compounded semiannually.

a. Find the future value if payments are made for three years.

Solution Find the future value of this ordinary annuity using .

In this case, PMT = 500, i = 0.05, and n = 6. This gives

This is calculated in a TI Graphing Calculator as shown below.

We could also find this same amount by adding the terms directly,

The six payments of $500 have earned $3400.96 – $3000 or $400.96 in interest over the life of the annuity.

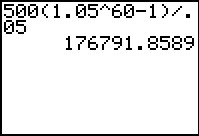

b. Find the future value if payments are made for 30 years.

Solution In this ordinary annuity, the term is much longer. The geometric series would have 30∙2 terms and it would not be practical to add the terms directly. However, if we set R = 500, i = 0.05, and n = 60 in the formula for the future value of an annuity, we get

This is calculated in a TI Graphing Calculator as shown below.

c. How much interest is earned over the 30 year term in part b?

Solution Over the term of the annuity, sixty payments of $500 are made for a total of $30,000. This yields $176,791.86 – $30,000 or $146,791.86 in interest.

The future value of an ordinary annuity formula assumes that the annuity starts out with a balance of zero. However, the annuity may have an existing balance and the payments are added to that amount. In this case, the balance grows according to the compound interest formula. The payments grow according to the future value of the annuity. The sum of these amounts is the future value of both investments combined.

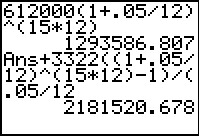

Example 3 Find the Future Value of a Retirement Account

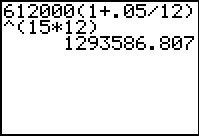

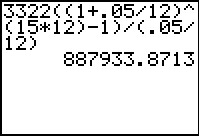

An employee’s retirement account currently has a balance of $612,000. Suppose the employee contributes $3322 at the end of each month. If the account earns a return of 5% compounded monthly, what will the future value of the account in 15 years?

Solution The original balance grows according to the compound interest formula, . The original amount is PV = 612,000, the interest rate per period is , and the number of periods over 15 years is n = 15 · 12.

This is calculated on a TI Graphing Calculator as shown below.

The future value of the payments into the annuity grow according to . For this account, the payment is PMT = 3322 and yields

This is calculated on a TI Graphing Calculator as shown below.

The sum of future value for the compounded amount and the future value of the annuity is $2,181,520.68.

We can combine the two amounts into a single formula that accounts for payments into an existing account that has some balance. In this context, the balance is called the present value. It corresponds to the value of the account at the time the payments commence.

Future Value of an Ordinary Annuity Whose Present Value Is Not Zero

If payments PMT are made to an ordinary annuity whose present value is PV, the future value is

If payments PMT are made from an ordinary annuity whose present value is PV, the future value is

We could have used the first formula to calculate the future value in Example 3,

We would calculate this amount on a TI Graphing Calculator in two steps.

In Examples 4, four of the five values in the future value formula for an ordinary annuity are known. This allows us to solve for the remaining value.

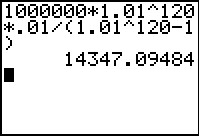

Example 4 Find the Payment from an Annuity

A savvy investor has accumulated $1,000,000 in an ordinary annuity. The annuity earns 4% interest compounded quarterly. She wishes to receive payments from the annuity each quarter for the next 30 years.

a. If the annuity will end up with no money in 30 years, what payment should she receive?

Solution Since the payments are made from an ordinary annuity, we’ll start from the future value of an ordinary annuity formula,

The annuity currently contains $1,000,000, so PV = 1,000,000. The investor wants the value of the annuity to be $0 in 30 years. This means FV = 0. Substitute these values, the interest rate per period , and the number of periods n = 4 · 30 to yield

To solve for the payment PMT, simplify and isolate the payment:

This is calculated in a TI Graphing Calculator as shown below.

The quarterly payment is $14,347.09.

The payment has been rounded down to insure all of the payments are equal. This will leave a small amount of money in the annuity at the end of 30 years. However, you could also round up if you realize the last payment might be different from the earlier payments.

b. The investor wishes to leave a balance in the annuity to leave to her heirs. If the annuity is to end contain $100,000 in 30 years, what payment should she receive?

Solution In this case, she wishes FV = 100,000. Change the future value to this amount an solve for the payment in

This is calculated in a TI Graphing Calculator as shown below.

Reducing the payment by $434.71 insures that the annuity will contain $100,000 in 30 years.